Fill Your Oklahoma 200 Form

Fill Your Oklahoma 200 Form

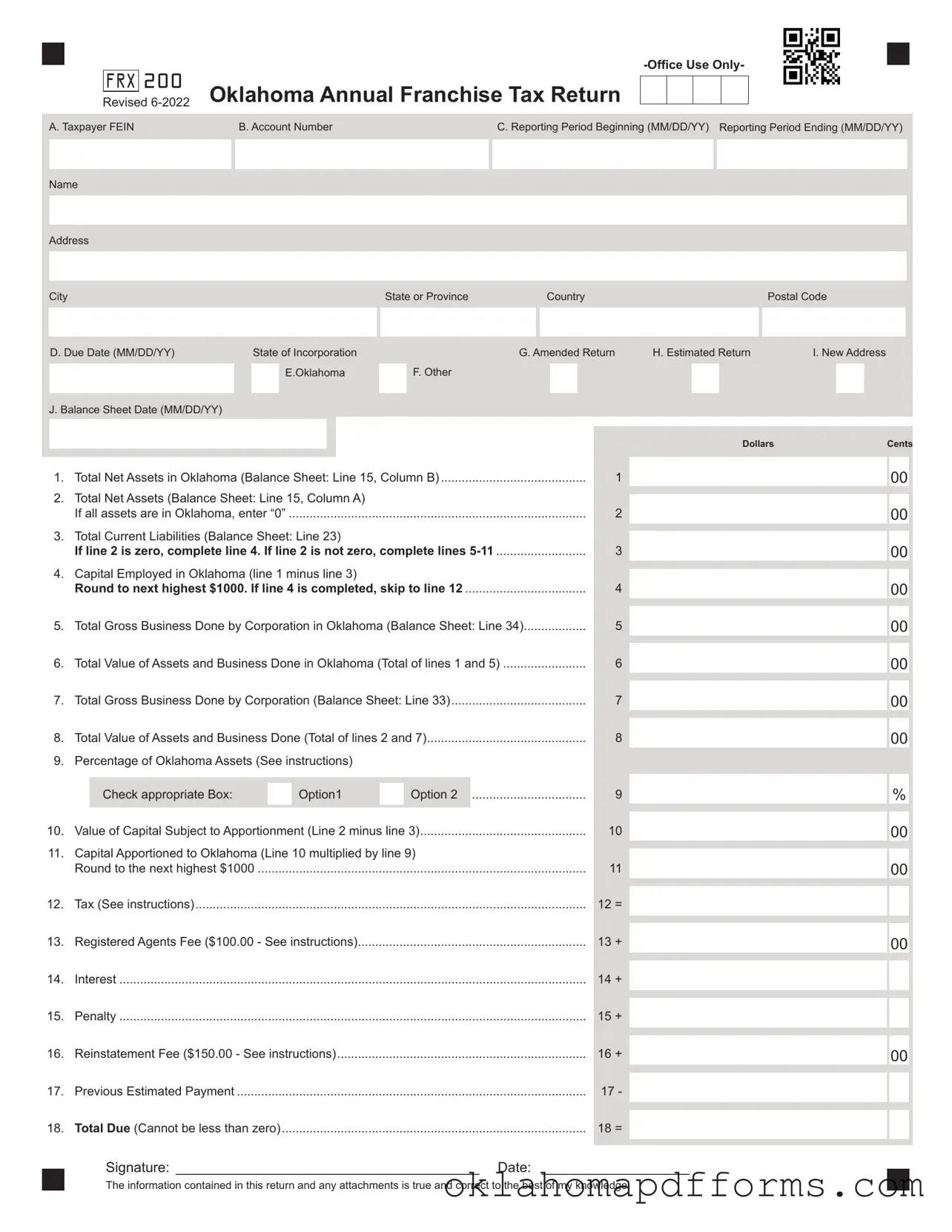

The Oklahoma 200 form, officially known as the Annual Franchise Tax Return, serves as a critical document for corporations operating within the state. This form must be completed by all corporations organized under Oklahoma laws or those qualified to do business in the state, including foreign entities. Key components of the form include the taxpayer's Federal Employer Identification Number (FEIN), account number, and the reporting period, which specifies the time frame for which the tax is being calculated. The due date for submission is also crucial, as late filings incur penalties and interest. The form requires detailed financial information, such as total net assets, current liabilities, and capital employed in Oklahoma, which helps determine the franchise tax owed. Additionally, corporations must provide information about their current officers, ensuring that the state has up-to-date records of corporate leadership. The form also includes schedules for related companies and current debt, which are essential for transparency and compliance. Understanding the Oklahoma 200 form is vital for any corporation, as it not only fulfills legal obligations but also ensures that businesses remain in good standing with the state tax authorities.

405 521 2122 - Your eligibility will be assessed based on the information provided on this form.

Oklahoma Use Tax - This exemption certificate does not cover all organizations; only designated types are eligible.

To facilitate the transfer of vehicle ownership, it is essential to utilize the Arizona Motor Vehicle Bill of Sale form effectively. This document not only details the buyer and seller information but also includes vital vehicle specifications, making it an indispensable tool for a seamless process. For further guidance on completing this form, you can refer to arizonapdfforms.com/motor-vehicle-bill-of-sale/, which offers additional resources and insights.

Oklahoma Nonresident Filing Requirements - Swelling and crepitus in the knee are evaluated during the physical assessment.

What is the Oklahoma 200 form?

The Oklahoma 200 form, also known as the Annual Franchise Tax Return, is a document that corporations must file to report their franchise tax liability to the state of Oklahoma. It is required for all corporations organized under Oklahoma law or doing business in Oklahoma, unless specifically exempted by statute. The form includes financial information and details about the corporation's officers.

Who needs to file the Oklahoma 200 form?

Every corporation organized under Oklahoma law or qualified to do business in Oklahoma must file the Oklahoma 200 form. This includes associations, joint stock companies, and business trusts. Foreign corporations doing business in Oklahoma are also required to file, along with paying a registered agent fee of $100.00.

When is the Oklahoma 200 form due?

The Oklahoma 200 form is due on July 1st of each year. If the corporation has filed a Franchise Election Form (Form 200-F), the due date may differ. If the form is not submitted by September 15th, the tax becomes delinquent, and penalties and interest may apply.

How is the franchise tax calculated?

The franchise tax is calculated based on the corporation's balance sheet at the end of the preceding income tax year. The tax rate is $1.25 per $1,000 of capital allocated or employed in Oklahoma. Corporations must consider both property owned and business done in Oklahoma when determining their tax liability.

What happens if the franchise tax is less than $250?

If the calculated franchise tax is $250 or less, the corporation is exempt from paying the tax. However, a “no tax due” Oklahoma 200 form must still be filed, and a schedule of corporate officers is required. The $100 registered agent fee still applies for foreign corporations.

What information is required on the Oklahoma 200 form?

The form requires various pieces of information, including the corporation's Federal Employer Identification Number (FEIN), account number, reporting period, and financial data such as total net assets and current liabilities. Additionally, a list of current corporate officers, including their names and Social Security numbers, must be included.

What are the penalties for late filing?

Late filings incur a penalty of 10% of the tax due, along with interest of 1.25% per month on the unpaid amount. If the form is not filed by the due date, the corporation may also face additional fees and complications with its standing in Oklahoma.

Can the Oklahoma 200 form be filed online?

Yes, the Oklahoma 200 form can be filed online through the Oklahoma Taxpayer Access Point (OkTAP). This platform allows corporations to file their franchise tax returns, submit officer listings, and pay associated fees conveniently.

What should be done if there is an error on the form?

If there is an error on the Oklahoma 200 form, the corporation should file an amended return. It is important to ensure that all information is accurate to avoid penalties and ensure compliance with state regulations.

Completing the Oklahoma 200 form requires careful attention to detail to ensure accuracy and compliance with state regulations. This process involves gathering essential information about your corporation, including financial data and officer details. Following the steps outlined below will help streamline the completion of the form.

After completing the Oklahoma 200 form, ensure that it is submitted by the due date to avoid any penalties. Filing can be done online through the Oklahoma Taxpayer Access Point or by mailing the completed form to the appropriate tax office. Keeping copies of the submitted documents for your records is also advisable.

The Oklahoma 200 form shares similarities with the IRS Form 1120, which is the U.S. Corporation Income Tax Return. Both documents require corporations to report their financial activities and tax obligations. The Oklahoma 200 focuses on franchise tax, whereas Form 1120 addresses federal income tax. Each form includes sections for reporting income, assets, and liabilities, ensuring that corporations provide a comprehensive overview of their financial status. Additionally, both forms require a signature to certify the accuracy of the information provided, highlighting the importance of accountability in corporate financial reporting.

Another comparable document is the California Form 100, the California Corporation Franchise or Income Tax Return. Like the Oklahoma 200, this form is used to calculate franchise tax obligations for corporations operating within the state. Both forms necessitate detailed financial disclosures, including balance sheets and income statements. However, the California Form 100 is tailored to California's tax laws and rates, while the Oklahoma 200 adheres to Oklahoma's specific requirements. This illustrates how state forms can mirror one another while still reflecting unique state tax structures.

The Texas Franchise Tax Report serves as a third similar document. This report is required for businesses operating in Texas and is used to calculate the franchise tax owed to the state. Much like the Oklahoma 200 form, the Texas report requires businesses to provide information about their revenue, assets, and liabilities. Both forms emphasize transparency and accountability, ensuring that corporations accurately report their financial health to state authorities. The key difference lies in the tax rates and specific calculations mandated by each state, which can lead to varying tax liabilities for similar businesses.

Understanding the significance of a bill of sale is essential for those engaging in property transactions. For a comprehensive overview, check out this guide on a detailed bill of sale template.

Lastly, the New York State Corporation Franchise Tax Return is another document that aligns with the Oklahoma 200 form. This return requires corporations to report their income and calculate the franchise tax owed to New York State. Both forms necessitate detailed financial information, including balance sheets and income statements, to ensure accurate tax assessments. While the Oklahoma 200 focuses on franchise tax based on capital employed in the state, the New York return may incorporate different metrics for tax calculation, reflecting the diverse approaches states take in taxing corporations.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

FRX |

200 |

Oklahoma Annual Franchise Tax Return |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

Revised |

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

A. Taxpayer FEIN |

|

B. Account Number |

|

|

|

|

C. Reporting Period Beginning (MM/DD/YY) Reporting Period Ending (MM/DD/YY) |

||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

City |

|

|

|

|

|

|

|

|

|

|

|

|

State or Province |

|

Country |

|

|

|

|

|

|

|

|

Postal Code |

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

D. Due Date (MM/DD/YY) |

|

|

State of Incorporation |

|

|

|

|

G. Amended Return |

|

|

H. Estimated Return |

I. New Address |

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

E.Oklahoma |

|

F. Other |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

J. Balance Sheet Date (MM/DD/YY) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Dollars |

Cents |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. |

|

Total Net Assets in Oklahoma (Balance Sheet: Line 15, Column B) |

|

|

|

|

1 |

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||

2. |

|

Total Net Assets (Balance Sheet: Line 15, Column A) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

If all assets are in Oklahoma, enter “0” |

|

|

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||

3. |

|

Total Current Liabilities (Balance Sheet: Line 23) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

3 |

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||

|

|

|

If line 2 is zero, complete line 4. If line 2 is not zero, complete lines |

.......................... |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

4. |

|

Capital Employed in Oklahoma (line 1 minus line 3) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||

|

|

|

Round to next highest $1000. If line 4 is completed, skip to line 12 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

5. |

|

Total Gross Business Done by Corporation in Oklahoma (Balance Sheet: Line 34) |

5 |

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

6. |

|

Total Value of Assets and Business Done in Oklahoma (Total of lines 1 and 5) |

6 |

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

7. |

|

Total Gross Business Done by Corporation (Balance Sheet: Line 33) |

|

|

|

|

7 |

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

8. |

|

Total Value of Assets and Business Done (Total of lines 2 and 7) |

|

|

|

|

8 |

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||

9. |

|

Percentage of Oklahoma Assets (See instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

% |

|

|

|

|

|

Check appropriate Box: |

|

|

|

|

Option1 |

|

Option 2 |

|

|

|

|

|

|

|

9 |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

................................. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

10. |

|

................................................Value of Capital Subject to Apportionment (Line 2 minus line 3) |

|

|

|

10 |

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||||

11. |

|

Capital Apportioned to Oklahoma (Line 10 multiplied by line 9) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

|||||||||||||||||||

|

|

|

Round to the next highest $1000 |

|

|

|

|

|

|

|

|

11 |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

12. |

|

Tax (See instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12 = |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

................................................................................................................. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

13. |

|

Registered Agents Fee ($100.00 - See instructions) |

|

|

|

|

|

|

|

|

13 + |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||

14. |

|

Interest |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 + |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

15. |

|

Penalty |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 + |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

16. |

|

Reinstatement Fee ($150.00 - See instructions) |

|

|

|

|

|

|

|

|

16 + |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

00 |

|

||||||||||||||||

17. |

|

Previous Estimated Payment |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17 - |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

..................................................................................................... |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

18. |

|

Total Due (Cannot be less than zero) |

|

|

|

|

|

|

|

|

18 = |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Signature: _______________________________________ |

Date: ___________________ |

|

|

|

|

|

|||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||

|

|

|

|

|

The information contained in this return and any attachments is true and correct to the best of my knowledge. |

|

|

|

|

|

||||||||||||||||||||||||||

|

|

|

|

|

Oklahoma Annual Franchise Tax Return |

|

|

||

|

|

|

FRX |

200 |

|

|

|||

|

|

|

|

|

|||||

|

|

|

|

|

Schedule A: Current Officer Information |

|

|

||

|

|

Page 2 |

|

|

|||||

|

|

|

|

|

|

|

|||

|

|

|

|

|

NOTE: Inclusion of Officers Is Mandatory. |

|

|

||

|

Taxpayer Name |

|

FEIN |

Account Number |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Corporate Officers Effective as of  Are as Follows:

Are as Follows:

(Date)

Example: Reporting period 07/01/2016 –

Schedule A: Current Officer Information

Enter the current officers effective date. The officers listed below should be those whose term was in effect as of June 30. Be sure to include names, addresses, and Social Security Numbers. A letter will be sent to all officers listed advising them they have been identified as an officer of the filing corporation. Officers listed in error will be advised to contact the corporation, not the Oklahoma Tax Commission to resolve. Officers may be updated or corrected when filing your annual franchise return via OkTAP.

|

1. First Name |

|

Middle Initial |

Last Name |

|

Social Security Number |

||

|

|

|

|

|

|

|

|

|

|

Home Address (street and number) |

|

|

|

|

|

Daytime Phone (area code and number) |

|

|

|

|

|

|

|

|

|

|

|

City |

State or Province |

Country |

Postal Code |

Title |

|||

|

|

|

|

|

|

|

|

|

|

2. First Name |

|

Middle Initial |

Last Name |

|

Social Security Number |

||

|

|

|

|

|

|

|

|

|

|

Home Address (street and number) |

|

|

|

|

|

Daytime Phone (area code and number) |

|

|

|

|

|

|

|

|

|

|

|

City |

State or Province |

Country |

Postal Code |

Title |

|||

|

|

|

|

|

|

|

|

|

|

3. First Name |

|

Middle Initial |

Last Name |

|

Social Security Number |

||

|

|

|

|

|

|

|

|

|

|

Home Address (street and number) |

|

|

|

|

|

Daytime Phone (area code and number) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

State or Province |

Country |

Postal Code |

Title |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. First Name |

|

Middle Intial |

Last Name |

|

Social Security Number |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Home Address (street and number) |

|

|

|

|

|

Daytime Phone (area code and number) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

State or Province |

Country |

Postal Code |

Title |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Please include Social Security Numbers of officers.

All returns, applications, and forms required to be filed with the Oklahoma Tax Commission (Commission) in the administration of this State’s tax laws shall bear the Federal Employer’s Identification Number(s), the Taxpayer Identification Number, and/or other gov- ernment issued identification number of the person, firm, or corporation filing the item and of all persons required by law or agency rule to

be named or listed.

[Source: Amended at 32 Ok Reg 1330, eff

FRX 200

Page 3

Oklahoma Annual Franchise Tax Return

Schedules B, C and D

Taxpayer Name |

FEIN |

|

|

|

|

This page contains Schedules B, C, and D for the completion of Form 200: Oklahoma Annual Franchise Tax Return. Attach additional pages if further space is needed on Schedules C and D.

Schedule B

General Information (to be completed in detail)

If the business is not a “corporation,” list the type of business structure, the date of formation, and county in which filed.

Name and address of Oklahoma “registered agent”

Name of parent company if applicable: |

|

|

|

|

FEIN: |

|

||||||

Percent of outstanding stock owned by the parent company, if applicable: |

|

|

|

% |

|

|

|

|||||

In detail, please list the nature of business: |

|

|

|

|

|

|

|

|||||

• Amount of authorized capital stock or shares: |

|

|

|

|

|

|

||||||

(a) Common: |

|

shares, par/book value of each share |

$ |

|

$ |

|

|

|||||

(b) First Preferred: |

|

shares, par/book value of each share |

$ |

|

$ |

|

|

|||||

• Total capital stock or shares issued and outstanding at the end of fiscal year: |

|

|

|

|

|

|

||||||

(a) Common: |

|

shares, par/book value of each share |

$ |

|

$ |

|

|

|||||

(b) First Preferred: |

shares, par/book value of each share |

$ |

$ |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule C

Related Companies: Subsidiaries and Affiliates

•subsidiaries (Companies in which you own 15 percent or more of the outstanding stock)

Name of Subsidiary |

|

FEIN |

|

Percentage Owned (%) |

|

Financial Investment ($) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

•affiliates (Companies related other than by direct stock ownership)

Name of Affiliate |

|

FEIN |

|

How related? |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule D |

|

|

|

|

|

|

|

|

Details of Current Debt shown on Balance Sheet |

|

Balance remaining of |

||||||

|

|

|

|

|

|

Original Amount |

amounts payable within 3 |

|

Name of Lender |

Original Date of Issuance Maturity Date |

of Instrument |

years of Date of Issuance |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FRX 200

Page 4

Oklahoma Annual Franchise Tax Return

Balance Sheet

Taxpayer Name |

FEIN |

As of the Last Income Tax Year Ended: (MM/DD/YY) |

|

|

|

|

|

|

This page contains the Balance Sheet which completes Form 200: Oklahoma Annual Franchise Tax Return.

Column A

Assets |

Total Everywhere as per |

|

|

|

Books of Account. |

|

If all Property is in |

|

Oklahoma, |

|

Do Not Use this Column. |

Column B

Total in Oklahoma

as per Books

of Account.

Liabilities and

Stockholders’

Equity

Column C

Total Everywhere as per

Books of Account.

1.Cash .......................................

2.Notes and accounts receivable

3.Inventories..............................

4.Government obligations and other bonds............................

5.Other current assets

(attach schedule)....................

6.Total Current Assets

(add lines

7.Mortgage and real estate loans

8.Other investments

(attach schedule)....................

9.(a) Building .............................

(b)Less accumulated depreciation........................

10.(a) Fixed depreciable assets .

(b)Less accumulated depreciation.......................

11.(a) Depletable assets.............

(b)Less accumulated depletion............................

12.Land......................................

13.(a) Intangible assets .............

(b)Less accumulated amortization......................

14.Other assets .........................

15.Net Assets ...........................

(Lines:

16.

(a)From parent company.....

(b)From subsidiary company

(c)From affiliated company .

17.Bank holding company stock in subsidiary bank .......

18.TOTAL ASSETS...................

(Lines:

19.Accounts payable ....................

20.Accrued payables ....................

21.Indebtedness payable three years or less after issuance

(see schedule D) .....................

22.Other current liabilities.............

23.Total Current Liabilities.........

(Lines:

24.

(a)To parent company.............

(b)To subsidiary company.......

(c)To affiliated company..........

25.Indebtedness maturing and payable in more than three years from the date of issu- ance.........................................

26.Loans from stockholders not payable within three years.......

27.Other liabilities.........................

28.Capital Stock

(a)Preferred stock....................

(b)Common Stock....................

29.

30.Retained earnings ...................

31.Other capital accounts.............

32.Total Liabilities and Stockholders’ Equity.............

(Lines:

33.Total gross business done everywhere

(sales and service) ................

(from income tax return)

34.Total gross business

done in Oklahoma

(sales and service) ................

(from income tax return)

Form 200 - Page 5

Oklahoma Annual Franchise Tax Return Information

• Requirement for Filing Return

Every corporation organized under the laws of this state, or qualified to do or doing business in Oklahoma in a corporate or organized

capacity by virtue or creation of organization under the laws of this state or any other state, territory, district, or a foreign country, including

associations, joint stock companies and business trusts as defined by Oklahoma statutes unless exempt by statutes must file an Annual Franchise Tax Return Form 200.

The term “doing business” means and includes every act, power, or privilege exercised or enjoyed in this state as an incident to do or by virtue of powers and privileges acquired by the nature of all organizations falling within the purview of the Franchise Tax Code.

All Foreign

on Line 13 of the Form 200.

The maximum annual franchise tax is $20,000.00. Maximum filers should complete and file Form 200 including a schedule of current corporate officers and balance sheet.

If a taxpayer computes the franchise tax due and determines that it amounts to $250.00 or less, the taxpayer is exempt from the tax and a

“no tax due” Form 200 is required to be filed. A schedule of corporate officers must still be filed and, for foreign corporations, the $100.00 registered agents fee is still due.

Applications for refunds must include copies of related Oklahoma Income Tax Returns. The use of the correct corporate name and FEIN on your return and all correspondence will facilitate in timely processing and handling.

• Time for Filing and Payment Information

Oklahoma Franchise Tax is due and payable July 1st of each year unless a Franchise Election Form

NOTE: Effective November 1, 2017, corporations who remit the maximum amount of $20,000.00 in the preceding tax year, the tax will be due and payable on May 1st of each year and delinquent if not paid on or before June 1st. These corporations are not eligible to file Form

If the Charter or other instrument is suspended, a fee of $150.00 is required for reinstatement. (Line 16 of Form 200.)

If you wish to make an election to change your filing frequency, or to file using the Oklahoma Corporate Income Tax Form 512 or

than July 1.

• Franchise Tax Computation

The basis for computing Oklahoma Franchise Tax is the balance sheet as shown by your books of account at the close of the last preceding

income tax accounting year, or electing to change filing to match the due date of the corporate income tax, the balance sheet for that corporate tax year.

The franchise tax for corporations doing business both within and outside of Oklahoma, is computed on the proportion to which property owned, or property owned and business done, within Oklahoma, bears to total property owned, or total property owned and total business done everywhere.

“Property owned” is the book value of the assets. For the purpose of determining apportionment as between Oklahoma and elsewhere, liabilities are not to be deducted from gross assets.

The term “business done” means and includes the engaging in any activity or the performing of any act or acts in this state that constitutes the doing or transacting of business. Business done in Oklahoma includes sales shipped from Oklahoma to another state in which the corporation is not doing business.

Oklahoma franchise (excise) tax is levied and assessed at the rate of $1.25 per $1,000.00 or fraction thereof on the amount of capital allocated or employed in Oklahoma.

• Online Filing

Oklahoma Taxpayer Access Point (OkTAP) makes it easy to file and pay. Visit us at tax.ok.gov to file your Franchise Tax Return, Officer

Listings, Balance Sheets and Franchise Election Form

Form 200 - Page 6

First Step...

Complete Balance Sheet and Schedules B, C & D

(Must be returned with annual return)

Line 1 (through 3) Cash, notes, accounts receivable, and inventories are to be reported at book value.

Line 4 United States, municipal, commercial and other bonds owned by the corporation.

Line 5 Prepaid expenses and deferred charges are to be included as assets at book value.

Line 8 Stock or other evidence of ownership in subsidiary organiza- tions as shown on the corporations books of account.

Lines 9b, 10b, 11b. If accumulated depreciation and depletion appear to be excessive, the excess may be disallowed.

Line 13 Patents, trademarks, copyrights, etc., and franchises are to

be included as assets to the extent of their cost. In the case of a definite term franchise, the cost thereof may be amortized

over its life. Goodwill is an asset and should be shown at book value. All intangibles including cash, are to be apportioned wholly to Oklahoma unless a commercial or business location for the intangibles has been established elsewhere.

Line 14 Life insurance, where the reporting taxpayer is beneficiary, is to be shown at cash surrender value.

Line 15 Total net amount of lines 6 through 14. Line 18 Total lines 15,16, and 17.

Line 20 Reserves for taxes are allowed to the extent such taxes are unpaid. Deferred credits are included in capital employed un- less they can be shown to be actual liabilities.

Line 21 Current liability includes indebtedness payable in three (3) years or less after issuance.

Line 26 Stockholder loans must be repaid within three years of cre- ation to be considered a current liability. Contingent assets or liabilities should not be included unless fully explained and the condition under which they become actual is clearly set forth.

Line 32 Total lines 23 through 31. The amounts as shown by the books of account shall be the measure of value of the assets

and liabilities, except when the items on the books of account are in error or lack sufficient detail to truly reflect the amount

of capital invested and employed in the business.

Second Step...

Complete the Oklahoma Annual Franchise Tax Return

Item A Place the taxpayer FEIN in Block A.

Item B Enter the Account number issued by the Oklahoma Tax Commission beginning with FRX followed by ten digits. If no number has been issued, leave blank.

Item C • Place the beginning and ending reporting period (MM/DD/

YY)for the Franchise Tax license year for which you are re- porting in Block C. Example: For returns due July 1, 2016 the reporting period beginning would be 07/01/16. The reporting

period ending would be 06/30/17.

•The reporting period for corporations which have filed Form

Item D Place the due date (MM/DD/YY) in Block D.

Item E Place an “X” in the box if you are incorporated in the State of Oklahoma.

Item F Place an “X” in the box if you are incorporated in a state other than Oklahoma.

Item G Place an “X” in the box if you are filing an amended return.

Item H Place an “X” in the box if you have not completed a year end balance sheet and are therefore filing an estimated return. You must file an estimated return and remit tax due.

Item I Place an “X” in the box if your mailing address has changed. Write your new address in the space provided.

Item J Enter your balance sheet date (MM/DD/YY) of your most

recent income tax accounting year. Do NOT leave blank. If the corporation has not completed its first taxable year enter June

30 of the current year as the balance sheet date.

(Continued from lower left column)

Lines 1 through 11 (except 9) are derived from your balance sheet. Put the date of the balance sheet in box J.

Line 9 (Percent of Oklahoma Assets)

Select which option you will use to determine the apportion- ment of Oklahoma assets.

Option 1: Percent of Oklahoma assets and business done to total assets and business done. (line 6 divided by line 8). Round to six decimal points.

Option 2: Percent of Oklahoma assets to total net assets (line 1 divided by line 2). Round to six decimal points.

Line 12 (Tax)

Compute tax at $1.25 per $1,000.00 of capital. (Either line 4 or line 11) If tax is more than $20,000.00 enter $20,000.00 on line 12. If your return is due July 1, 2014 or later, you are

exempt from paying tax if your tax liability is $250.00 or less, however, a return must still be filed.

Line 13 (Registered Agent Fee)

If the corporation originated in a state other than Oklahoma, the Oklahoma Secretary of State charges an annual regis-

tered agent fee of $100.00 and is collected on the franchise tax return.

Annual Franchise Tax Return”. Line 14 (Interest)

If this return is postmarked after the due date the tax is sub- ject to 1.25% interest per month from the due date until it is paid. Multiply the amount in Line 12 by .0125 for each month the report is late.

Line 15 (Penalty)

Tax not paid by the original due date is subject to a penalty of 10%. Multiply the amount in Line 12 by .10 to determine the penalty.

Line 16 (Reinstatement Fee)

If your corporate charter has been suspended, you must meet all outstanding filing and payment obligations in order to be

reinstated. Effective July 1, 2017, a $150.00 reinstatement fee

is also required. Only one reinstatement fee is required even if multiple past due returns are being filed.

Line 17 (Previous Estimated Franchise Payment)

•Enter any estimated franchise tax paid with Form 200

•If filing an amended return, enter any franchise tax paid with the original return and amounts paid after it was filed.

Line 18 (Total Due)

Add the amounts from lines 12 through 16, subtract any entry on line 17, and enter total on line 18. Amount on line 18 can- not be less than zero.

Third Step...

Schedule A Officer Information

Enter the effective date of officers. Refer to the example on Schedule A. Failure to provide this information could result in the corporation being suspended.

Fourth Step...

Mail this return to the address below. Include your return, payment made payable to Oklahoma Tax Commission, balance sheet, and schedules A, B, C, and D.

Please Mail To:

Oklahoma Tax Commission

PO Box 26850

Oklahoma City, OK

Phone Number for Assistance – 405.521.3160

Mandatory inclusion of Social Security and/or Federal Employer’s

Identification numbers is required on forms filed with the Oklahoma

Tax Commission (OTC) pursuant to 68 of the Oklahoma Statutes and regulations thereunder, for identification purposes, and are deemed to be part of the confidential files and records of the OTC.

The OTC is not required to give actual notice to taxpayers of changes in state laws.

(Continued top of right column)

The Oklahoma 200 form is a crucial document for corporations operating in Oklahoma, serving as the Annual Franchise Tax Return. However, it is often accompanied by several other forms and documents that provide additional information or fulfill specific requirements. Below is a list of these documents, each described briefly to clarify their purpose and importance.

Understanding these accompanying documents is essential for ensuring compliance with Oklahoma tax laws. By properly completing and submitting the Oklahoma 200 form along with the relevant schedules and forms, corporations can avoid penalties and ensure their operations remain in good standing with state authorities.

When filling out the Oklahoma 200 form, there are several important considerations to keep in mind to ensure compliance and accuracy. Here are key takeaways that can guide you through the process:

By following these takeaways, individuals and corporations can navigate the complexities of the Oklahoma 200 form with greater ease and confidence.