Fill Your Oklahoma 501 Form

Fill Your Oklahoma 501 Form

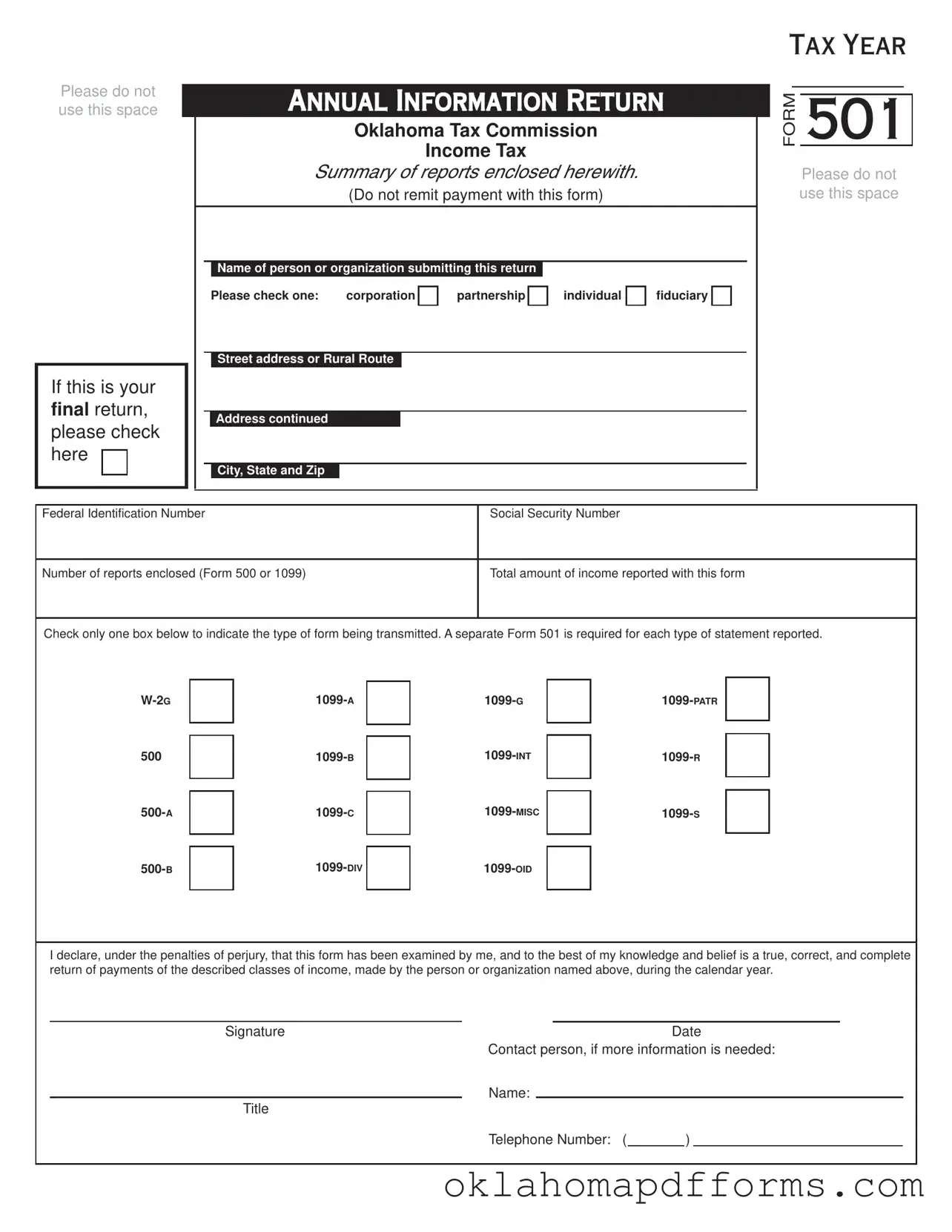

The Oklahoma 501 form serves as an essential document for various entities reporting income payments to the Oklahoma Tax Commission. This form is primarily used by corporations, partnerships, individuals, and fiduciaries to summarize and submit information about payments made during the tax year. It is crucial for payors, including churches, charitable organizations, and government entities, to understand their reporting obligations. The form requires details such as the name of the submitting entity, federal identification number, and the total income reported. Payors must indicate the type of income statement being submitted, which can include various forms like W-2G, 1099-MISC, and others. The Oklahoma Tax Commission mandates that this return be filed by February 28 of the following year, with specific exceptions for certain types of payments. It is important to note that no payment should be remitted with the form itself. Additionally, the 501 form includes a declaration of accuracy, underscoring the responsibility of the submitter to ensure the information is correct and complete. Understanding the requirements and deadlines associated with the Oklahoma 501 form is vital for compliance and to avoid potential penalties.

Oklahoma Tax Id Number - The Oklahoma Income Tax amount on line 4 is not the amount withheld from you.

Oklahoma Employment Security Commission Hq Oklahoma City, Ok - Direct Deposit can simplify your financial management during unemployment.

The California Articles of Incorporation form is a crucial document used by businesses to legally establish themselves as corporations within the state. It outlines basic information about the company, including its name, purpose, and the structure of its stock. For those looking for more information on the process and requirements, legalformspdf.com provides valuable resources. Submitting this form is a foundational step for companies aiming to operate in California, marking the beginning of their legal and financial journey.

Oklahoma Unemployment Tax Id Number - The report requires the contribution rate for the calendar quarter to be listed as a decimal.

What is the Oklahoma 501 form?

The Oklahoma 501 form is an annual information return used to report various types of income payments made by individuals or organizations. This form is submitted to the Oklahoma Tax Commission and includes details about payments such as interest, dividends, and gambling winnings. It serves as a summary of reports enclosed, such as Forms 500 and 1099, and must be completed accurately to comply with state tax regulations.

Who is required to submit the Oklahoma 501 form?

All payors, including churches, charitable organizations, labor unions, and any tax-exempt entities, are required to submit the Oklahoma 501 form if they have made qualifying payments. This includes payments made to individuals, trusts, estates, corporations, and partnerships. If the payments total $750 or more in a calendar year, they must be reported using this form.

What are the due dates for submitting the Oklahoma 501 form?

The Oklahoma 501 form, along with any accompanying reports, must be submitted to the Oklahoma Tax Commission by February 28 of the year following the tax year. However, if you are required to withhold income tax from royalty payments made to nonresident royalty owners, the deadline is January 31. Similarly, pass-through entities have specific deadlines related to their income tax returns.

What types of payments must be reported on the Oklahoma 501 form?

Payments that need to be reported include interest, rent, dividends, annuities, gambling winnings, and other fixed or determinable gains. For residents, payments of $750 or more must be reported. For nonresidents, payments of $750 or more from property owned or business conducted in Oklahoma also require reporting. Specific rules apply to production payments and professional payments, which should be reviewed carefully.

Can I submit the Oklahoma 501 form without payment?

Yes, you should not remit payment with the Oklahoma 501 form. The form is strictly for reporting income payments and does not require any payment to be submitted along with it. Ensure that all information is accurate and complete before submission to avoid any penalties.

Where should I send the Oklahoma 501 form?

The completed Oklahoma 501 form and any accompanying reports should be mailed to the Oklahoma Tax Commission at the following address: 2501 North Lincoln Blvd., Oklahoma City, Oklahoma 73194-0009. Make sure to send it well before the due date to ensure timely processing.

Completing the Oklahoma 501 form requires careful attention to detail. After filling out the form, ensure that all necessary reports are enclosed before submitting it to the Oklahoma Tax Commission.

The Oklahoma 501 form is similar to the IRS Form 1099 series, which includes various forms used to report different types of income. Each 1099 form serves a specific purpose, such as reporting interest income (1099-INT), dividend income (1099-DIV), or miscellaneous income (1099-MISC). Like the Oklahoma 501, these forms require the payer to report income paid to individuals or entities, ensuring that the IRS receives accurate information about earnings. Both the 501 form and the 1099 series help maintain transparency and compliance with tax laws, allowing the government to track income and enforce tax obligations.

When engaging in any financial transactions, it's vital to utilize the correct documentation to ensure clarity and legal standing. One such document is the Bill of Sale, which can be crucial in confirming the exchange of asset ownership. For more information or to access a template, you can visit legalpdf.org, where you'll find resources to assist in formalizing your transactions effectively.

Another document similar to the Oklahoma 501 form is the IRS Form W-2. This form is used by employers to report wages paid to employees and the taxes withheld from those wages. Just like the 501 form, the W-2 provides a summary of payments made during the year and is essential for tax reporting purposes. Both forms require the payer to submit the information to the respective tax authorities and provide copies to the recipients, ensuring that income is accurately reported and taxed accordingly.

The Oklahoma 500 form also shares similarities with the 501 form. This form is used to report income from various sources, including business income, rents, and royalties. Both forms require the reporting of income amounts and are submitted to the Oklahoma Tax Commission. The 500 form is specifically tailored for individuals and entities reporting their total income, while the 501 form focuses on the reporting of payments made to others, creating a comprehensive view of income flows within the state.

The IRS Form 1042-S is another document that resembles the Oklahoma 501 form. This form is used to report income paid to foreign persons, including nonresident aliens and foreign corporations. Like the 501 form, the 1042-S requires the payer to report payments made and any withholding tax applied. Both forms serve to ensure compliance with tax regulations and help the government track income that may be subject to different tax rules based on residency status.

Lastly, the Oklahoma Form 500-A is comparable to the 501 form, as it is used to report payments made to nonresident individuals or entities. This form focuses on income subject to withholding tax, similar to the 501 form's requirement for reporting various payments. Both forms are crucial for ensuring that the appropriate taxes are withheld and reported to the Oklahoma Tax Commission, thereby promoting compliance with state tax laws.

Please do not use this space

If this is your final return, please check here

ANNUAL INFORMATION RETURN

Oklahoma Tax Commission

Income Tax

Summary of reports enclosed herewith.

(Do not remit payment with this form)

Name of person or organization submitting this return |

|

|

||

Please check one: |

corporation |

partnership |

individual |

fiduciary |

Street address or Rural Route

Address continued

City, State and Zip

TAX YEAR

________

FORM 501

Please do not use this space

Federal Identification Number |

Social Security Number |

|

|

Number of reports enclosed (Form 500 or 1099) |

Total amount of income reported with this form |

|

|

Check only one box below to indicate the type of form being transmitted. A separate Form 501 is required for each type of statement reported.

|

|

|

||||

500 |

|

|

|

|

||

|

|

|

||||

|

|

|

||||

|

|

|

||||

|

|

|

||||

|

|

|

||||

|

|

|

|

|||

|

|

|

|

|||

|

|

|

|

|||

|

|

|

|

|

|

|

I declare, under the penalties of perjury, that this form has been examined by me, and to the best of my knowledge and belief is a true, correct, and complete return of payments of the described classes of income, made by the person or organization named above, during the calendar year.

Signature |

Date |

||||

|

Contact person, if more information is needed: |

||||

|

Name: |

|

|

|

|

Title |

|

|

|

||

|

Telephone Number: ( |

|

) |

|

|

FORM 501 INSTRUCTIONS

WHO SHALL REPORT...

All payors, including but not limited to churches, charitable organizations, labor unions, lodges, fraternities, sororities, school districts, state, county and municipal departments, cooperatives and any other tax exempt organization, shall report these payments.

DUE DATES...

This return together with the reports enclosed must be forwarded so as to reach the Oklahoma Tax Commission before February 28 of the succeeding calendar year except where indicated below.

•Every remitter, required to withhold income tax from royalty payments made to nonresident royalty owners, shall furnish this return together with either Forms

•Every

PAYMENTS TO BE REPORTED WHEN PAID TO RESIDENTS...

All persons (individuals, trusts, estates, corporations and partnerships) acting as payor, and including lessees, mortgagors of real and personal property, employers, officers and employees of the state or any political subdivision thereof, should report the following payments when these payments amount to $750 or more in the calendar year: interest, rent, dividends, annuities, gambling winnings, or other fixed or determinable or periodical gains, profits or income.

PRODUCTION PAYMENT RULES (RESIDENT • NONRESIDENT)...

The Oklahoma Tax Commission requires the reporting of “production payments” made to individuals, corporations, partnerships, trusts or estates whether made to a resident or nonresident. For purposes of Title 68 O.S. 2369, production payments means payments of proceeds generated from mineral interests in this state, including, but not limited to, a lease bonus, delay rental, royalty and working interest payment, and overriding royalty interest payment. Income from real property should be reported only when the property is located within Oklahoma, whether the recipient is a resident or nonresident. Amounts to report: $750 or more except $10 or more for royalties. However, all payments with Oklahoma withholding must be reported. State code “OK” must be entered in box 17 of form

DIVIDEND OR INTEREST PAYMENTS...

Corporations paying to individuals interest on bonds, mortgages, deeds of trusts and other similar obligations or dividend payments, should report these when they exceed $100; other persons (individuals, trusts, estates and partnerships) should report interest payments of $750 or more, when paid to an individual. Brokers or agents in stocks, bonds, and security or stock transactions will report, on Form 500, the total amount of commodity or security sales or the total market value of the securities exchanged for the customer, when they were $25,000 or more in the calendar year. This includes banks which handle orders for depositors or custodian accounts.

NONRESIDENTS...

Persons making payments to nonresident individuals, partnerships, trusts, corporations or estates of fixed or determinable income, from property owned, business or trade carried on in Oklahoma or gambling winnings won in Oklahoma, totaling $750 or more in the calendar year should report such payments. Also see production payment rules for nonresidents.

PROFESSIONAL PAYMENTS...

Persons making payments to professional individuals should report them when they amount to $750 or more and are made to an Oklahoma resident or to a nonresident providing professional services within the State of Oklahoma.

Oklahoma requires withholding from distributions made to nonresident members (partners, members, shareholders or beneficiaries) of

GENERAL INFORMATION...

The foregoing instructions are in conformity with the provisions of the Oklahoma statutes, requiring information returns to be filed in accordance with rules and regulations prescribed and adopted by the Tax Commission. The Oklahoma Tax Commission is not required to notify taxpayers of changes in any state tax law.

MAILING ADDRESS...

Please forward this return and accompanying reports to: Oklahoma Tax Commission, 2501 North Lincoln Blvd., Oklahoma City, Oklahoma

The Oklahoma 501 form is an important document for reporting various types of income to the Oklahoma Tax Commission. Along with this form, there are several other documents that are commonly used. Each serves a specific purpose in the reporting process. Below is a list of these documents, along with a brief description of each.

Understanding these forms and their specific functions can help ensure compliance with Oklahoma tax regulations. Accurate reporting is crucial to avoid penalties and ensure that all income is properly accounted for. If you have questions about any of these forms, consulting a tax professional may be beneficial.

Filling out and using the Oklahoma 501 form requires attention to detail and adherence to specific guidelines. Here are key takeaways to consider:

It is essential to ensure that all information is accurate and complete to avoid penalties. Review the guidelines carefully before submitting the form.