Fill Your Oklahoma 511Tx Form

Fill Your Oklahoma 511Tx Form

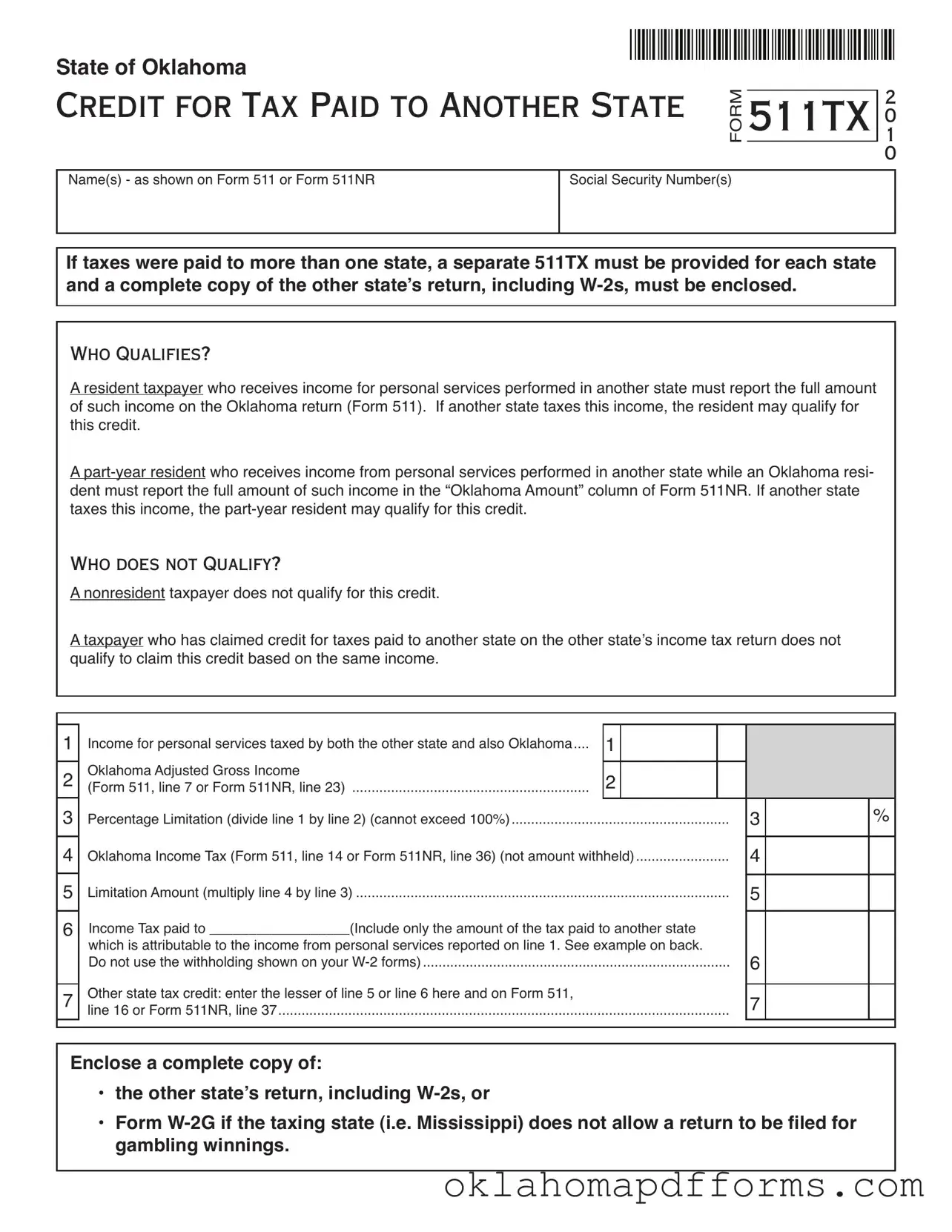

The Oklahoma 511Tx form serves as a crucial tool for residents and part-year residents who have earned income from personal services in another state and have faced taxation on that income from both Oklahoma and the other state. This form allows eligible taxpayers to claim a credit for taxes paid to another state, helping to alleviate the burden of double taxation. To qualify for this credit, individuals must report their total income from personal services on their Oklahoma tax return, specifically on Form 511 for residents or Form 511NR for part-year residents. However, it is important to note that nonresident taxpayers do not qualify for this credit. For those who do qualify, the process involves providing detailed information about the income earned and the taxes paid, including a complete copy of the other state's tax return and any relevant W-2 forms. The form includes specific lines to calculate the amount of income taxed by both states and the corresponding tax liability. Additionally, taxpayers must ensure that they do not claim this credit if they have already accounted for the taxes paid to another state on that state’s income tax return. By understanding the requirements and processes outlined in the 511Tx form, individuals can navigate their tax obligations more effectively and potentially reduce their overall tax liability.

Oklahoma Title Transfer - There's a specific fee for certified copies, which are sometimes necessary for court proceedings.

The Washington Articles of Incorporation form is essential for anyone looking to formally set up a corporation in the state, providing necessary details such as the corporation's name and purpose, as well as information about its incorporators and registered agent. To further assist you in this important process, you can visit legalpdf.org for additional resources and guidance.

Oklahoma State Campus - 4-H members learn through community service and hands-on project experiences.

What is the purpose of the Oklahoma 511Tx form?

The Oklahoma 511Tx form is used to claim a credit for taxes paid to another state. This credit is available to Oklahoma residents and part-year residents who earn income from personal services in another state and are taxed on that income by both states. The form helps to prevent double taxation on the same income.

Who qualifies to use the 511Tx form?

Residents of Oklahoma who receive income for personal services performed in another state can qualify for this credit. This also applies to part-year residents who earned income from personal services while residing in Oklahoma. Both types of taxpayers must report the full amount of that income on their Oklahoma tax return (Form 511 or Form 511NR) to be eligible for the credit.

What documentation is required when submitting the 511Tx form?

When filing the 511Tx form, taxpayers must include a complete copy of the tax return from the other state, along with copies of all W-2 forms. If the other state does not allow a return for certain types of income, such as gambling winnings, a Form W-2G should be enclosed instead. This documentation is essential for processing the credit claim.

Are there any taxpayers who do not qualify for the credit?

Nonresident taxpayers do not qualify for the credit. Additionally, if a taxpayer has already claimed a credit for taxes paid to another state on that state’s income tax return, they cannot claim the credit on the Oklahoma 511Tx form for the same income. This rule helps ensure that taxpayers do not receive multiple credits for the same tax payment.

To fill out the Oklahoma 511Tx form, gather the necessary information and documents before starting. This includes your Social Security number, details of income from personal services, and tax information from the other state. Make sure to have a complete copy of the other state’s tax return and any W-2 forms ready to include with your submission.

The Oklahoma 511Tx form is similar to the California Form 540, which allows taxpayers to claim a credit for taxes paid to another state. Both forms require individuals to report income earned in other states and provide documentation of taxes paid. In California, residents who earn income in other states must report this income on their state tax returns. If they have paid taxes to another state on that income, they can claim a credit to avoid double taxation. The process involves including a copy of the other state’s tax return along with the California return, mirroring the requirements outlined in the Oklahoma 511Tx form.

Another comparable document is the New York Form IT-112-R, which serves a similar purpose. New York residents who work in another state can claim a credit for taxes paid to that state. The form requires taxpayers to report their total income, including that earned outside New York, and to provide proof of taxes paid. Like the Oklahoma 511Tx, the New York form aims to prevent double taxation on income that has already been taxed by another jurisdiction. Taxpayers must submit a copy of the other state's tax return, ensuring consistency in documentation requirements.

The Texas Form 00-102, known as the Texas Franchise Tax Report, also shares similarities with the Oklahoma 511Tx. While Texas does not impose a personal income tax, businesses operating in multiple states may need to report income and taxes paid elsewhere. The Texas form requires businesses to disclose their total income and any taxes paid to other states, enabling them to account for their tax liabilities accurately. Although the focus is on business income rather than personal income, the underlying principle of avoiding double taxation remains a common thread.

For a smooth trailer ownership transfer, consider utilizing a comprehensive Trailer Bill of Sale template available online. This document not only formalizes the transaction but also protects the interests of both parties involved. You can access the template by visiting this link for a Trailer Bill of Sale.

In Illinois, the Schedule CR form is utilized for claiming a credit for taxes paid to other states. Illinois residents who earn income outside of Illinois must report that income and can claim a credit for taxes paid to other states. The requirements for documentation and calculation are akin to those found in the Oklahoma 511Tx form. Taxpayers must provide a copy of the other state’s tax return and detail the amount of income earned and taxes paid, reinforcing the commitment to prevent double taxation.

The Massachusetts Form 1-NR/PY is another document that parallels the Oklahoma 511Tx. This form is specifically for part-year residents and nonresidents who earn income in Massachusetts and other states. Similar to the Oklahoma form, it allows taxpayers to claim a credit for taxes paid to another state. The process involves reporting income from personal services and including documentation of taxes paid, ensuring that individuals are not taxed twice on the same income.

The Florida Form DR-15, while primarily a sales tax return, also addresses tax credits for businesses that operate in multiple states. Businesses in Florida that pay taxes in other states can report these taxes and claim credits. This form, while different in its primary focus, still reflects the principle of preventing double taxation, which is a key aspect of the Oklahoma 511Tx form. The documentation requirements also align, as businesses must provide proof of taxes paid to other jurisdictions.

Another relevant document is the Pennsylvania Schedule G, which allows residents to claim a credit for taxes paid to other states. Pennsylvania taxpayers who earn income in other states must report this income and can claim a credit for taxes paid, similar to the Oklahoma 511Tx. The form requires detailed reporting of income and taxes paid, ensuring that residents are not subjected to double taxation on their earnings.

The Virginia Form 760, which is the individual income tax return, also includes provisions for claiming credits for taxes paid to other states. Virginia residents who earn income in other states must report this income and can claim a credit for taxes paid, mirroring the Oklahoma 511Tx process. The requirement to submit documentation, such as copies of the other state’s tax returns, reinforces the shared goal of preventing double taxation.

Lastly, the New Jersey Form NJ-1040 allows residents to claim a credit for taxes paid to other states. New Jersey taxpayers who work outside the state must report their income and can claim a credit for taxes paid to those states. The documentation requirements and the calculation of the credit align closely with those of the Oklahoma 511Tx form. Both forms aim to ensure fairness in taxation and prevent residents from facing double taxation on their income.

State of Oklahoma

CREDIT FOR TAX PAID TO

Name(s) - as shown on Form 511 or Form 511NR

|

|

FORM |

511TX |

10 |

ANOTHER STATE |

|

|

2 |

|

|

|

|

||

|

|

|

0 |

|

|

Social Security Number(s) |

|

|

|

|

|

|

||

|

|

|

|

|

If taxes were paid to more than one state, a separate 511TX must be provided for each state and a complete copy of the other state’s return, including

WHO QUALIFIES?

A resident taxpayer who receives income for personal services performed in another state must report the full amount of such income on the Oklahoma return (Form 511). If another state taxes this income, the resident may qualify for this credit.

A

WHO DOES NOT QUALIFY?

A nonresident taxpayer does not qualify for this credit.

A taxpayer who has claimed credit for taxes paid to another state on the other state’s income tax return does not qualify to claim this credit based on the same income.

|

|

|

|

|

|

|

|

1 |

Income for personal services taxed by both the other state and also Oklahoma.... |

1 |

|

|

|

|

|

|

Oklahoma Adjusted Gross Income |

|

|

|

|

|

|

2 |

2 |

|

|

|

|

|

|

(Form 511, line 7 or Form 511NR, line 23) |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

3 |

Percentage Limitation (divide line 1 by line 2) (cannot exceed 100%) |

|

|

|

3 |

|

% |

|

|

|

|

|

|||

4 |

Oklahoma Income Tax (Form 511, line 14 or Form 511NR, line 36) (not amount withheld) |

4 |

|

|

|||

|

|

|

|

|

|

|

|

5 |

Limitation Amount (multiply line 4 by line 3) |

|

|

|

5 |

|

|

|

|

|

|

|

|||

6 |

Income Tax paid to __________________(Include only the amount of the tax paid to another state |

|

|

|

|||

|

which is attributable to the income from personal services reported on line 1. See example on back. |

|

|

|

|||

|

Do not use the withholding shown on your |

|

|

|

6 |

|

|

|

Other state tax credit: enter the lesser of line 5 or line 6 here and on Form 511, |

|

|

|

|

|

|

7 |

|

|

|

7 |

|

|

|

line 16 or Form 511NR, line 37 |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Enclose a complete copy of:

•the other state’s return, including

•Form

FORM 511TX - CREDIT FOR TAX PAID TO ANOTHER STATE

TITLE 68 O.S. SECTION 2357(B)(1) AND RULE

INSTRUCTIONS

This schedule, a complete copy of the other state’s tax return and copies of all

Line 1

Include only the amount of wages, salaries, commissions and other pay for personal services which is being taxed by Oklahoma and also the other state. Gambling winnings are considered income from personal services for purposes of this credit.

Example 1. John is an Oklahoma resident, filing Form 511. He worked and owned rental property in an- other state. The other state’s return shows wages of $20,000 and rental income of $10,000. Line 1 would be $20,000, the amount of income from personal services included in his Okla- homa adjusted gross income and taxed by another state.

Example 2. Beth is a

Line 6

Include only the amount of the tax paid to another state which is attributable to the income from personal services reported on line 1. Do not use the withholding shown on your

Example: personal services (from line 1) total income from another state

Xtotal tax paid to another state = tax paid to another state (not withholding tax)

Example 1. Bill is an Oklahoma resident, filing Form 511. The other state’s return shows $5,000 in wages,

$7,000 in rental income from the other state, and $8,000 from the sale of a house located in the other state. The other state’s total tax liability is $546. Since only the $5,000 in wages is income from personal services subject to tax in both states, line 6 would be computed as fol-

lows: |

$5,000 X $546 = $137 |

|

$20,000 |

Example 2. (continued from Line 1, Example 2 above)

The other state taxed all of Beth’s wage income; however, only the portion she earned while an Oklahoma resident was taxed by both states (see line 1). Her other state’s total tax liability was $754. Beth determines the portion of the other state’s tax that is attributable to the por- tion of her wage income which is being taxed in both states as follows:

$22,500 X $754 = $566 $30,000

The Oklahoma 511Tx form is essential for residents who have paid taxes to another state on income earned from personal services. Along with this form, several other documents are commonly used to ensure accurate tax reporting and compliance. Below is a list of these forms and documents, along with brief descriptions of their purposes.

Using these forms correctly helps ensure compliance with tax regulations and maximizes potential credits. Always keep copies of submitted forms for your records, and consult with a tax professional if you have questions about your specific situation.

When filling out the Oklahoma 511Tx form, it is essential to keep in mind several important points to ensure accuracy and compliance.