Fill Your Oklahoma 512 X Form

Fill Your Oklahoma 512 X Form

The Oklahoma 512-X form is an essential document for corporations seeking to amend their income tax returns in the state of Oklahoma. This form allows businesses to make necessary adjustments to their previously filed returns, ensuring compliance with state tax laws. It requires corporations to provide key information, including their federal employer identification number, business code, and type of business. Additionally, the form necessitates the inclusion of a copy of the federal return, especially if the amended return is a result of a federal audit. Taxpayers must calculate their Oklahoma taxable income, which involves detailing gross income and applicable deductions. The form also outlines various credits available to reduce tax liability, such as the Investment/New Jobs Credit and the Credit for Biomedical Research Contribution. Furthermore, it mandates the reporting of any tax due or refunds expected, with specific instructions for direct deposit of refunds. Completing the 512-X form accurately is crucial, as it requires a declaration of truthfulness under penalties of perjury, emphasizing the importance of diligence in the amendment process.

Oklahoma Tax Commission Forms - Consolidated entities must ensure all subsidiaries or related entities are accurately reported.

Having a legal document like a Medical Power of Attorney is crucial for individuals who want to prepare for unexpected health situations. By appointing a trusted person to make healthcare decisions on their behalf, they can ensure that their medical preferences are respected, even when they cannot express them. To learn more about creating this important form, visit https://arizonapdfforms.com/medical-power-of-attorney/, which provides valuable information on the process and its significance.

Small Claims Court Tulsa - Understanding the importance of each section can streamline the legal process and enhance clarity.

What is the purpose of the Oklahoma 512-X form?

The Oklahoma 512-X form is used by corporations to file an amended income tax return in Oklahoma. This form allows businesses to correct previously filed returns, whether due to changes in income, deductions, or credits. It is essential for ensuring that the tax obligations are accurately reported and that any overpayments or underpayments are addressed. By filing this form, corporations can maintain compliance with state tax laws and possibly receive refunds for overpaid taxes.

Who needs to file the Oklahoma 512-X form?

What documents must be submitted along with the 512-X form?

How can a corporation receive a refund after filing the 512-X form?

What are the consequences of not filing an amended return when required?

Filling out the Oklahoma 512 X form is an essential process for corporations needing to amend their income tax return. Completing this form accurately ensures compliance with state tax regulations. Below are the steps to guide you through the process of filling out the form.

The Oklahoma 512-X form is similar to the IRS Form 1120X, which is the Amended U.S. Corporation Income Tax Return. Both forms allow corporations to amend their previously filed tax returns. When a corporation discovers errors or omissions in its original return, it can use Form 1120X to correct those mistakes at the federal level. This form requires the corporation to explain the reasons for the amendment and provide any supporting documentation, similar to the requirements of the Oklahoma 512-X form.

Another document that resembles the Oklahoma 512-X form is the IRS Form 1139, which is used to apply for a quick refund of an unused credit. Corporations that have overpaid their taxes or have credits that were not utilized can file this form to receive a refund. Like the 512-X, Form 1139 requires supporting documentation, including a copy of the original return, to substantiate the claim for a refund.

The Oklahoma Corporate Franchise Tax Return (Form 200) is also similar to the 512-X form. While the 512-X is specifically for amending income tax returns, Form 200 is used to report corporate franchise taxes. Both forms require detailed financial information about the corporation and may involve adjustments based on prior filings. Both documents emphasize the importance of accurate reporting and compliance with state tax laws.

Form 501 is another related document, as it is the Oklahoma Corporation Income Tax Return. Corporations must file this form annually to report their income and calculate their tax liability. Similar to the 512-X, Form 501 requires detailed financial information and may involve adjustments if the corporation has made errors in its previous filings.

The IRS Schedule A, which is part of the Form 1120, is akin to the Oklahoma 512-X as it outlines the income and deductions for corporations. Both documents require a breakdown of gross income and allowable deductions, allowing for a clear picture of the corporation's financial status. Accurate reporting on both forms is essential to determine the correct tax liability.

Form 511CR is another similar document that pertains to Oklahoma tax credits. Corporations can claim various credits that may reduce their tax liability. Like the 512-X, this form requires documentation to support the claims for credits, ensuring that the corporation complies with state tax regulations.

Form 1099 is also relevant, as it reports various types of income other than wages, salaries, and tips. Corporations may need to include information from Form 1099 when filing the 512-X if they have received income that affects their tax calculations. Both forms require careful attention to detail to ensure accurate reporting of income.

Additionally, the Oklahoma Schedule B is comparable to the 512-X, as it is used to compute taxable income for unitary businesses. Both documents require detailed calculations and may involve apportioning income based on the corporation's operations within and outside of Oklahoma. This ensures that the tax liability is accurately determined based on the corporation's activities.

The Oklahoma Business Personal Property Tax Return is similar in that it requires businesses to report their personal property for tax purposes. While the 512-X focuses on income tax, both forms necessitate accurate reporting of a business's financial situation and compliance with state tax laws, ensuring that all applicable taxes are paid.

For those looking to document their trailer transactions effectively, the convenient Trailer Bill of Sale template is an excellent resource. This document is designed to ensure a smooth transfer of ownership while safeguarding the interests of both the buyer and seller involved.

Lastly, the Oklahoma Sales Tax Return can be seen as analogous to the 512-X form. Both documents require businesses to report financial information and comply with state tax obligations. While the 512-X focuses on income tax, the Sales Tax Return addresses sales tax, yet both require a clear understanding of the business's financial activities and accurate reporting to avoid penalties.

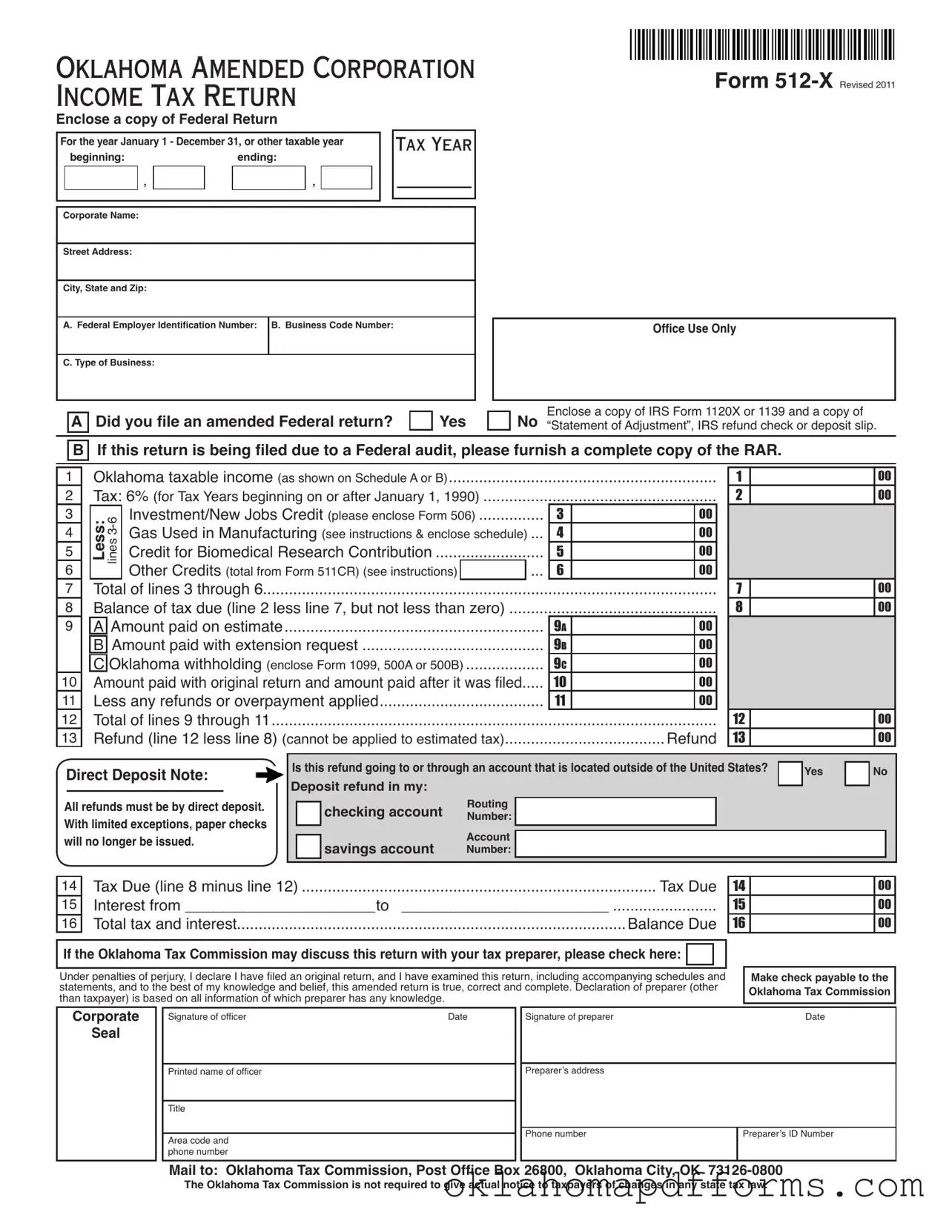

OKLAHOMA AMENDED CORPORATION INCOME TAX RETURN

Enclose a copy of Federal Return

For the year January 1 - December 31, or other taxable year |

|

TAX YEAR |

||||||||||

|

beginning: |

|

|

ending: |

|

|

|

|

||||

|

|

, |

|

|

|

, |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Corporate Name:

Street Address:

City, State and Zip:

A. Federal Employer Identiication Number: B. Business Code Number:

C. Type of Business:

Form

Ofice Use Only

A Did you ile an amended Federal return? |

|

Yes |

|

No |

Enclose a copy of IRS Form 1120X or 1139 and a copy of |

|

|

||||

|

|

“Statement of Adjustment”, IRS refund check or deposit slip. |

B If this return is being iled due to a Federal audit, please furnish a complete copy of the RAR.

1

2

3

4

5

6

7

8

9

10

11

12

13

|

Oklahoma taxable income (as shown on Schedule A or B) |

|

|

|

|||||

|

Tax: 6% (for Tax Years beginning on or after January 1, 1990) |

|

|

|

|||||

|

Less: lines |

Investment/New Jobs Credit (please enclose Form 506) |

3 |

|

00 |

||||

|

Gas Used in Manufacturing (see instructions & enclose schedule) |

... |

4 |

|

00 |

||||

|

Credit for Biomedical Research Contribution |

5 |

|

00 |

|||||

|

Other Credits (total from Form 511CR) (see instructions) |

|

|

... |

6 |

|

00 |

||

|

|

|

|

|

|

||||

|

Total of lines 3 through 6 |

|

|

|

|||||

|

Balance of tax due (line 2 less line 7, but not less than zero) |

|

|

|

|||||

|

A |

Amount paid on estimate |

9A |

|

00 |

||||

|

B Amount paid with extension request |

9B |

|

00 |

|||||

|

C Oklahoma withholding (enclose Form 1099, 500A or 500B) |

9C |

|

00 |

|||||

|

Amount paid with original return and amount paid after it was iled |

|

10 |

|

00 |

||||

|

|

|

|

||||||

|

Less any refunds or overpayment applied |

11 |

|

00 |

|||||

|

.......................................................................................................Total of lines 9 through 11 |

|

|

|

|||||

|

Refund (line 12 less line 8) (cannot be applied to estimated tax) |

|

Refund |

||||||

1 |

|

00 |

|

|

|

2 |

|

00 |

|

|

|

|

|

|

7 |

|

00 |

|

|

|

8 |

|

00 |

|

|

|

|

|

|

12 |

|

00 |

|

|

|

13 |

|

00 |

|

|

|

Direct Deposit Note:

All refunds must be by direct deposit. With limited exceptions, paper checks will no longer be issued.

Is this refund going to or through an account that is located outside of the United States? |

|

Yes |

|

No |

||||||

|

|

|||||||||

Deposit refund in my: |

Routing |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||||

|

|

checking account |

|

|

|

|

|

|

|

|

|

|

Number: |

|

|

|

|

|

|

|

|

|

|

savings account |

Account |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

Number: |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

14

15

16

Tax Due (line 8 minus line 12) |

Tax Due |

Interest from ______________________to |

________________________ |

Total tax and interest |

Balance Due |

14

15

16

00

00

00

If the Oklahoma Tax Commission may discuss this return with your tax preparer, please check here:

Under penalties of perjury, I declare I have iled an original return, and I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, this amended return is true, correct and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Make check payable to the Oklahoma Tax Commission

Corporate

Seal

Signature of oficer |

Date |

|

Signature of preparer |

Date |

|

|

|

|

|

Printed name of oficer |

|

|

Preparer’s address |

|

|

|

|

|

|

Title |

|

|

|

|

|

|

|

|

|

|

|

|

Phone number |

Preparer’s ID Number |

Area code and |

|

|||

|

|

|

|

|

phone number |

|

|

|

|

Mail to: Oklahoma Tax Commission, Post Ofice Box 26800, Oklahoma City, OK

The Oklahoma Tax Commission is not required to give actual notice to taxpayers of changes in any state tax law.

|

Form |

|

|

|

|

|

|||

|

|

|

|

|

|

||||

|

SCHEDULE A |

Schedule A Column A is for all corporations. Schedule A, Column B is for corporations whose income |

|||||||

|

|

|

|

is all within Oklahoma and/or for corporations whose income is partly within and partly without Okla- |

|||||

|

Important: All applicable lines and |

homa (not unitary). Enclose a complete copy |

|

|

|

|

|

||

|

|

|

Column A |

|

Column B |

||||

|

schedules must be illed in. |

of your Federal return. (1120X,1139 or amended 1120) |

As reported on |

|

Total applicable |

||||

|

Gross Income (lines 1 through 11) |

|

|

Federal Return |

|

to Oklahoma |

|||

|

|

|

|

.......... |

1 |

|

|

|

|

|

1 |

Gross receipts or gross sales __________ (less: returns and allowances) |

|

|

|

|

|||

|

2 |

Less: Cost of goods sold |

2 |

|

|

|

|

||

|

3 |

Gross proit (line 1 minus line 2) |

3 |

|

|

|

|

||

|

4 |

Dividends |

4 |

|

|

|

|

||

|

5 |

Interest on obligations of the United States and U.S. Instrumentalities |

5 |

|

|

|

|

||

|

6 |

(a) |

Other interest |

6a |

|

|

|

||

|

|

(b) |

Municipal interest |

6b |

|

|

|

||

|

7 |

Gross rents |

7 |

|

|

|

|

||

|

8 |

Gross royalties |

8 |

|

|

|

|

||

|

9 |

(a) |

Net capital gains |

9a |

|

|

|

||

|

|

(b) |

Ordinary gain or [loss] |

9b |

|

|

|

||

|

10 |

Other income (enclose schedule) |

10 |

|

|

|

|

||

|

11 |

Total income (add lines 3 through 10) |

11 |

|

|

|

|

||

|

|

Deductions (lines 12 through 27) |

|

|

|

|

|

||

|

12 |

Compensation of oficers |

12 |

|

|

|

|

||

|

13 |

Salaries and wages |

13 |

|

|

|

|

||

|

14 |

Repairs |

14 |

|

|

|

|

||

|

15 |

Bad debts |

15 |

|

|

|

|

||

|

16 |

Rents |

16 |

|

|

|

|

||

|

17 |

Taxes |

17 |

|

|

|

|

||

|

18 |

Interest |

18 |

|

|

|

|

||

|

19 |

Charitable contributions |

19 |

|

|

|

|

||

|

20 |

Depreciation |

20 |

|

|

|

|

||

|

21 |

Depletion (see instructions below) |

21 |

|

|

|

|

||

|

22 |

Advertising |

22 |

|

|

|

|

||

|

23 |

.Pension, |

23 |

|

|

|

|

||

|

24 |

Employee beneit programs |

24 |

|

|

|

|

||

|

25 |

Domestic production activities deduction |

25 |

|

|

|

|

||

|

26 |

Other deductions (enclose schedule) |

26 |

|

|

|

|

||

|

27 |

Total Deductions (add lines 12 through 26) |

27 |

|

|

|

|

||

|

Totals (lines 28 through 30) |

|

|

|

|

|

|

||

|

28 |

Taxable income before net operating loss deductions and special deductions ... |

28 |

|

|

|

|

||

|

29 |

Less: (a) Net operating loss deduction (schedule) |

29a |

|

|

|

|||

|

|

|

(b) Special deductions |

............................................................................. |

29b |

|

|

|

|

|

30 |

Taxable income (line 28 minus lines 29a & b) Enter Column B on page 1, line 1 |

30 |

|

|

|

|

||

Note: Indicate method used to allocate expenses to Oklahoma and enclose schedule of computations.

Oklahoma Depletion in Lieu of Federal Depletion

Oklahoma depletion on oil and gas may be computed at 22% of gross income derived from each Oklahoma property during the taxable year but limited to 50% of the

net income from such property (computed without the allowance for depletion). Provided, for tax years beginning on or after January 1, 1997 and ending on or before December 31, 1999, and for tax years beginning on or after January 1, 2001 and ending on or before December 31, 2011, only major oil companies, as deined in 68 Oklahoma Statutes Section 288.2, when computing Oklahoma depletion shall be limited to 50% of the net income form each property. A depletion schedule by property must be enclosed with the return. Note: General and administrative expense (computed on basis of Oklahoma direct expense to total direct expense) must be deducted before applying the 50% test.

EXPLANATION OR REASON FOR AMENDED RETURN

(Enclose all necessary schedules, including RAR’s)

Form |

|

||||

SCHEDULE B |

Schedule B is for computation of Oklahoma taxable income |

|

|||

of a unitary enterprise. [Section 2358(A) (5)] Enclose a complete |

|

||||

|

|

|

copy of your Federal return. (1120X, 1139 or amended 1120) |

|

|

|

|

|

|

||

1 |

Net taxable income from Schedule A, Column A, line 30 |

|

|||

|

|||||

2 |

Add: (a) Taxes based on income |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

$ |

||

|

(b) |

. . . . . . . . . . . . . . . . . . . . . . . . .Federal net operating loss deduction |

|

||

|

(c) |

. . . . . . . . . . . . . . . . . . . .Unallowable deduction (enclose schedule) |

|

||

|

. . . . . . . . . . . . . . . . . . . . . . . . . .(d) ____________________________ |

|

|||

|

. . . . . . . . . . . . . . . . . . . . . . . . . .(e) ____________________________ |

|

|||

|

. . .(f) Total of lines 2a through 2e |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

||

3 |

Deduct all items separately allocated |

|

|

||

|

. . . . . . . . . . . . . . . . . . . . . . . . . .(a) ____________________________ |

$ |

|||

|

. . . . . . . . . . . . . . . . . . . . . . . . . .(b) ____________________________ |

|

|||

|

. . . . . . . . . . . . . . . . . . . . . . . . . .(c) ____________________________ |

|

|||

|

. . . . . . . . . . . . . . . . . . . . . . . . . .(d) ____________________________ |

|

|||

|

. . . . . . . . . . . . . . . . . . . . . . . . . .(e) ____________________________ |

|

|||

|

(f) |

. . .Total of lines 3a through 3e |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

|

|

(Note: Items listed in 2 and 3 above must be net amounts supported |

|

|||

|

by schedules showing source, location, expenses, etc.) |

|

|||

4 |

Net apportionable income . . |

. . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

|

5 |

. . . .Oklahoma’s portion thereof __________________%, from schedule below |

|

|||

6 |

Add or deduct items separately allocated to Oklahoma (enclose schedule) |

|

|||

|

. . . . . . . . . . . . . . . . . . . . . . . .(a) ____________________________________ |

$ |

|||

|

. . . . . . . . . . . . . . . . . . . . . . . .(b) ____________________________________ |

|

|||

|

. . . . . . . . . . . . . . . . . . . . . . . .(c) ____________________________________ |

|

|||

|

(d) Oklahoma net operating loss deduction (enclose schedule) |

|

|||

|

|

||||

7 |

. . . . . . . . . . . . . . . . . . . . .Oklahoma net income before tax (add lines 5 and 6) |

|

|||

8 |

Oklahoma accrued tax (divide line 7 by number for applicable year.) |

|

|||

9 |

Oklahoma taxable income, line 7 less line 8 (enter on page 1, line 1) |

|

|||

$

$

$

$

$

$

$

$

APPORTIONMENT FORMULA

1

2

3

4

5

6

Value of real and tangible personal property used in |

Column A |

|

Column B |

|

A divided by B |

|

the unitary business (by averaging the value at the |

Total Within |

|

Total Within and |

|

Percent Within |

|

beginning and ending of the tax period). |

Oklahoma |

|

Without Oklahoma |

|

Oklahoma |

|

(a) Owned property (at original cost): |

|

|

|

|

|

|

(I) |

Inventories |

|

|

|

|

|

(II) |

Depreciable property |

|

|

|

|

|

(III) |

Land |

|

|

|

|

|

|

|

|

|

|

||

(IV) |

Total of section “a” |

|

|

|

|

|

|

|

|

|

|

||

(b)Rented property (capitalize at 8 times net rental paid)

(c) |

Total of sections “a” and “b” above |

$ |

|

$ |

|

% |

(a) |

Payroll |

|

|

|

|

|

(b) |

Less: Oficer salaries |

|

|

|

|

|

(c) |

Total (subtract oficer salaries from payroll) |

$ |

|

$ |

|

% |

Sales : |

|

|

|

|

|

|

(a)Sales delivered or shipped to Oklahoma purchasers: (I) Shipped from outside Oklahoma . . . . . . . . . . . .

(II) Shipped from within Oklahoma . . . . . . . . . . . . .

(b) |

Sales shipped from Oklahoma to: |

|

|

|

|

|

|

|

|

|

|

(I) The United States Government |

|

|

|

|

|

|

|

|

|

|

(II) Purchasers in a state or country where the |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

corporation is not taxable (i.e. under Public Law |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(c) |

Total of sections “a” and “b” |

$ |

|

|

$ |

|

% |

|||

If Revenue, Trafic Units or Miles Traveled is used rather than Sales, indicate here: |

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

Total percent (sum of items 1, 2 and 3) |

. |

. . . . . . . . . . . . . . . . . |

|

% |

||||||

Average percent (1/3 of total percent) (Carry to Schedule B, line 5) |

|

|

% |

|||||||

Form

This page must be completed. |

|

|

|

|

|

|

|

|

||

BALANCE SHEETS |

|

Beginning of taxable year |

|

End of taxable year |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(A) Amount |

|

(B) Total |

|

(C) Amount |

|

(D) Total |

|

1 |

Cash |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

Trade notes and accounts receivable |

|

|

|

|

|

|

|

|

|

|

(a) Less allowance for bad debts |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Inventories |

|

|

|

|

|

|

|

|

|

4 |

Gov’t obligations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

(a) U.S. and instrumentalities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

(b) State, subdivision, thereof, etc |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

5 |

Other current assets (enclose schedule) . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

6 |

Loans to shareholders |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

7 |

Mortgage and real estate loans |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

8 |

Other investments (enclose schedule) . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

9Buildings and other ixed depreciable assets

(a) Less accumulated depreciation . . . . . . .

10 |

. . . . . . . . . . . . . . . . . . . .Depletable assets |

|

|

|

|

|

|||

|

(a) Less accumulated depletion |

||||||||

|

|

||||||||

11 |

Land (net of any amortization) |

|

|

|

|

||||

12 |

. . . . .Intangible assets (amortization only) |

|

|

|

|

|

|

||

|

(a) Less accumulated amortization |

||||||||

13 |

Other assets (enclose schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

14 |

Total assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15 |

Accounts payable |

|

|

|

|

|

|

|

|

16 |

|

|

|

|

|

|

|

|

|

17 |

Other current liabilities (enclose schedule) . |

|

|

|

|

|

|

|

|

18 |

Loans from shareholders |

|

|

|

|

|

|

|

|

19 |

|

|

|

|

|

|

|

|

|

20 |

Other liabilities (enclose schedule) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

21 |

. . . . . . .Capital stock: (a) preferred stock |

|

|

|

|

|

|||

|

(b) common stock |

||||||||

22

23Retained

24Retained

25Adjustments to shareholder’s equity (enclose sch.)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

26 Less cost of treasury stock |

( |

|

) |

( |

) |

|||||||||

27 |

Total liabilities and shareholders equity . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

SCHEDULE OK |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Net income (loss) per books |

|

|

|

7 |

Income recorded on books this year not |

|

|

||||||

2 |

. . . . . . . . . . . . . . . . . . .Federal income tax |

|

|

|

|

included in this return (enclose schedule) |

|

|

||||||

3 |

Excess of capital losses over capital gains . |

|

|

|

|

(a) Tax exempt interest $________________ |

|

|

||||||

4 |

Taxable income not recorded on books this |

|

|

|

|

(b) Other |

|

$________________ |

|

|

|

|||

|

. . . . . . . . . . . . . . .year (enclose schedule) |

|

|

|

|

. . . . . . . . . . . . . . .(c) Total of lines 7a and 7b |

|

|

||||||

5 |

Expenses recorded on books this year not |

|

|

|

8 |

Deductions in this tax return not charged |

|

|

||||||

|

|

|

|

|

||||||||||

|

deducted in this return (enclose schedule) . |

|

|

|

|

against book income this year (enclose schedule) |

|

|

||||||

|

(a) Depreciation |

$ ___________________ |

|

|

|

|

|

(a) Depreciation $_____________________ |

|

|

||||

|

(b) Depletion |

$ ___________________ |

|

|

|

|

|

(b) Depletion |

$_____________________ |

|

|

|

||

|

(c) Other ___________________________ |

|

|

|

|

(c) Other ____________________________ |

|

|

||||||

|

________________________________ |

|

|

|

|

|

. . . . . . . . . . . . .(d) Total of lines 8a, 8b and 8c |

|

|

|||||

|

. . . . . . . . . . .(d) Total of lines 5a, 5b and 5c |

|

|

|

9 |

Total of lines 7c and 8d |

|

|

||||||

6 |

. . . . . . . . . .Total of lines 1 through 4 and 5d |

|

|

|

10 |

Net income: line 6 less line 9 |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SCHEDULE OK |

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

. . . . . . . . . . . .Balance at beginning of year |

|

|

5 |

Distributions: |

(a) |

Cash |

|

|

|||||

2 |

. . . . . . . . . . . .Net income (loss) per books |

|

|

|

|

|

(b) |

Stock |

|

|

||||

3 |

Other increases (enclose schedule) _____ |

|

|

|

|

|

(c) |

. . . . . . . . . . . . . . .Property |

|

|

||||

|

__________________________________ |

|

|

|

|

6 |

Other decreases (enclose sch.)___________ |

|

|

|||||

|

|

|

|

|

|

|

||||||||

|

__________________________________ |

|

|

|

|

|

____________________________________ |

|

|

|

||||

4 |

. . . . . . . . . . . . . . . .Total of lines 1, 2 and 3 |

|

|

|

7 |

. . . . . . . . . . . . . . . . . . . .Total of lines 5 and 6 |

|

|

||||||

|

|

|

|

|

|

|

8 |

Balance at end of year (line 4 less line 7) |

|

|

||||

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The Oklahoma 512-X form is an essential document for corporations looking to amend their income tax returns in Oklahoma. However, it often accompanies several other forms and documents to ensure a complete and accurate submission. Understanding these additional documents can make the process smoother and help avoid potential issues with the Oklahoma Tax Commission.

Submitting the Oklahoma 512-X form along with the appropriate supporting documents is vital for a successful amendment. By ensuring that all necessary forms are included, corporations can navigate the amendment process more effectively and minimize the risk of complications with their tax filings.

Filling out the Oklahoma 512 X form is a critical process for corporations needing to amend their income tax returns. Here are five key takeaways to keep in mind when using this form:

Understanding these key points can streamline the process of filing an amended return and help avoid potential issues with the Oklahoma Tax Commission.